Investment Accounts You Should Know About

Investment Accounts You Should Know About

With so many choices of different investment accounts, which should you choose?

Dear Sunday Investors:

Welcome to our fourth week of the Sunday Investor! To our new members, the format of this weekly newsletter will be a deep-dive into one investment-topic. This week, we will focus on the different types of investment accounts we can open to invest in the stock market. We will go into the advantages and disadvantages of each of these accounts as well as instructions on how to open them!

Read, enjoy and share with your network. Let’s all build wealth together.

Weekly Market Recap

By one of our reader’s requests, this will be the first edition of the “Weekly Market Recap” where we will go into some of the most important events that happened in the markets in the last week:

Coinbase releases NFT platform; Waitlist over 1M people in 48 hours. You can learn more and join the waitlist here

Energy prices continue to rise and brent oil prices hit $85/barrel for the first time since 2018

Bitcoin continued its rally and climb above $60,000 propelled by the perspective of a potential ETF approval

s")

Deciding Where to Put Your Money

Once you have outlined your personal investing goals, the next step is to decide which investment accounts to set up. Each investment account we will talk about here has its advantages and disadvantages, so lets jump right in.

Brokerage Account:

Max Contribution: No limit

Withdrawal Rules: No restrictions unless enforced by broker; must pay taxes on capital gains or taxable distributions

Mandatory Withdrawals: No rules

A brokerage account is one of the easiest and flexible accounts to open and begin investing with. There are no restrictions on contributions or withdrawals on this type of account. Investments made into a brokerage account are made with after-tax dollars, meaning with money that has already been taxed/deposited into your bank account like a work paystub.

When it comes to taxes, you are taxed on your profits and it depends on your income level and whether it was a long-term or short-term investment for the exact amounts.

As far as which brokerage to invest with, I would recommend TD Ameritrade, Charles Schwab, Fidelity, or Robinhood to get started.

Retirement Accounts:

Check out NerdWallet’s Retirement Calculator to track your plan for retirement

401(k) Account

Max Contribution (2021): $19,500 + $6,500 (catch-up contribution eligible) for individual; $57,000 total between individual + employer annually

Withdrawal Rules (2021): Money withdrawn before age 59.5 has a 10% additional tax

Mandatory Withdrawals (2021): Must begin withdrawing by 72 to avoid penalties

The 401k plan is the most popular retirement plan available to the average American. If you are offered 4%+ match for a 401k at your employer, you should absolutely take advantage of this!

It is also vital not only to start saving, but to start saving & investing EARLY!

Take This For Example:

Let’s say beginning at age 25, you begin contributing 10% of your $50,000 income to your 401(k) plan. If we assume an average annual rate of return on investment of 7% (a mix between stocks and bonds), you’ll have approximately $1.035 million dollars saved by the time you’re 65.

But if you wait until you’re 35, and begin contributing 10% of your $100,000 income, again assuming a 7% annual rate of return, you’ll have only a little over $980,000 by the time you reach 65.

Individual Retirement Account (IRA)

Max Contribution (2021): $6,000 + $1,000 (catch-up contribution eligible) for individual

Withdrawal Rules (2021): Money withdrawn before age 59.5 has a 10% additional tax

Mandatory Withdrawals (2021): Must begin withdrawing by 72 to avoid penalties

Traditional IRAs are tax-deferred accounts which means that, like a 401(k) account, you will not have to pay income taxes on the money that you contribute to the account. These taxes do not go away forever; You will end up paying taxes once you make withdrawals in retirement.

You can contribute up to $6,000 per year to a Traditional IRA or $7,000 per year if you are 50 or older.

In an IRA, if you withdrawal for an unqualified reason before age 59.5, you are hit with an additional 10% penalty on funds so it is important to invest wisely here.

Roth IRA

Max Contribution (2021): $6,000 + $1,000 (catch-up contribution eligible) for individual

Withdrawal Rules (2021): You can withdraw your Roth IRA contributions at any time, for any reason, with no tax or penalties. Earnings withdrawn before age 59.5 has a 10% additional tax on capital gains.

Mandatory Withdrawals (2021): None (taxes paid at time of contribution)

Roth IRAs are funded with money that you’ve already paid taxes on. Because you are paying taxes now as opposed to later, a Roth IRA can be great for investors who are currently in lower income-tax brackets and expect to earn (and spend) more in the future. If you are like me and investing in your 20s, this may describe you.

A Roth IRA can be great for investors who are currently in low income-tax brackets and expect to earn (and spend) more in the future.

Like a Traditional IRA, a Roth IRA has a $6,000 contribution limit. (And people over 50 years old can contribute an additional $1,000 each year.) Unlike a Traditional IRA, there are income limits on a Roth IRA. Currently, eligibility starts phasing out at $124,000 for single tax filers and $196,000 for joint tax filers so if you make more than these amounts then you cannot contribute to this account.

Pro Tip: Set-Up Recurring Deposits To Your Investment Accounts

Setting up recurring deposits helps you save without even thinking about it; set it and forget it. Example: If you want to contribute the max $6,000 contribution to your Roth IRA, set recurring deposits of $250 for 2 times a month.

I Have An Account Now, What Should I Invest In?

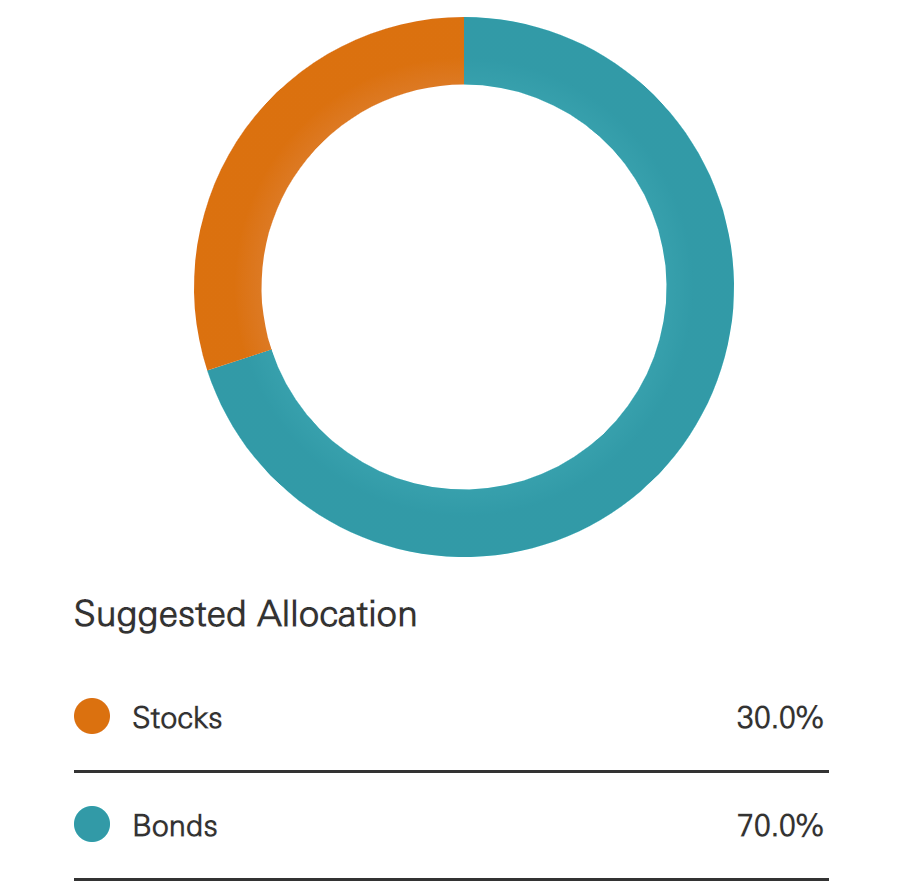

Everyone is different. That’s why it is important to get an idea of your appetite for risk by completing a Risk Tolerance Assessment like this one from Vanguard.

After completing an assessment like this, it will recommend a portfolio allocation for your stock market investing:

Example of how this could look:

Diversification:

In terms of choosing which investments go into your portfolio, an easy place to start is by looking through Vanguards ETFs which are pre-diversified funds with 30+ stocks that can be sector specific, or other categories like only international stocks, total market indexes, and much more.

For individual stock research, there is potential for higher returns, but that comes with higher risks as well. It is important to do your research wisely here. We will go into this in more detail in a following newsletter.

Where to Open An Account:

There are many places to get started with opening an account. I have broken the options down into 3 categories to make it easy to decide which makes most sense for you!

Biggest Names in the Game

Fidelity, TD Ameritrade, Charles Schwab, E*TRADE

These are the top names in investing. They offer commission free trading, educational content, high-quality customer support, and a simplistic UI for new investors. You are able to open a brokerage account, IRA, or Roth IRA on all of these.

Fin-Tech Companies

M1 Finance, Robinhood, WeBull

These are the up and coming Fin-Tech players in investing. These options also all offer commission free trading, and a very simplistic UI for new investors. An option like M1 Finance allow users to choose their own “basket” of up to 30 stocks to invest in for free. In all, each of these options have a differentiator that has allowed them to grow exponentially with the younger generations. Some of these platforms are more limited with accounts you can open. (Ex. Robinhood does not have IRA or Roth IRA options yet)

Check out my portfolio of 30 stocks on M1 Finance which is up over 66% in the last year: https://m1.finance/3KyfmfAE2yOf

Robo-Financial Advisors

Betterment, Wealthfront, Acorns, Titan

These are the top players for “no-touch investing”. What this means is that you take a risk tolerance quiz like the Vanguard quiz above, and these platforms automatically invest you in a diversified portfolio based on your risk tolerance. What is important to note here is that these platforms charge anywhere from .25%-1% of the money you put in your account for their services. These platforms are great if you do not want to worry about choosing individual stocks or manually diversifying your portfolio as the applications do this for you.

Next Week

Next week, we will continue our journey on investment research and different investment strategies within the stock market, or we could also head over to dig deeper into the world of NFT’s.

What do you want to see next? NFT’s, Stocks, Options, Crypto? Comment here what you want to see and I will make it happen:

Not financial or tax advice. The content in this newsletter is for informational purposes only. Every investment and trading move involves risk. Do your own research when making a decision.